Term Life vs Whole Life Insurance: What I Wish Someone Had Told Me Before I Signed That Policy

Here’s a stat that honestly blew my mind — according to LIMRA’s 2024 Insurance Barometer Study, about 42% of Americans don’t have any life insurance at all. And of the ones who do? A huge chunk of them don’t really understand what they bought. I was one of those people for years, and let me tell you, it cost me.

When I was 28, I walked into an insurance agent’s office thinking I’d be in and out in twenty minutes. I walked out with a whole life insurance policy that was eating $280 a month from my paycheck. Was it the right call? Spoiler alert — for my situation, absolutely not. So let’s break down the whole term life vs whole life insurance thing so you don’t make the same mistakes I did.

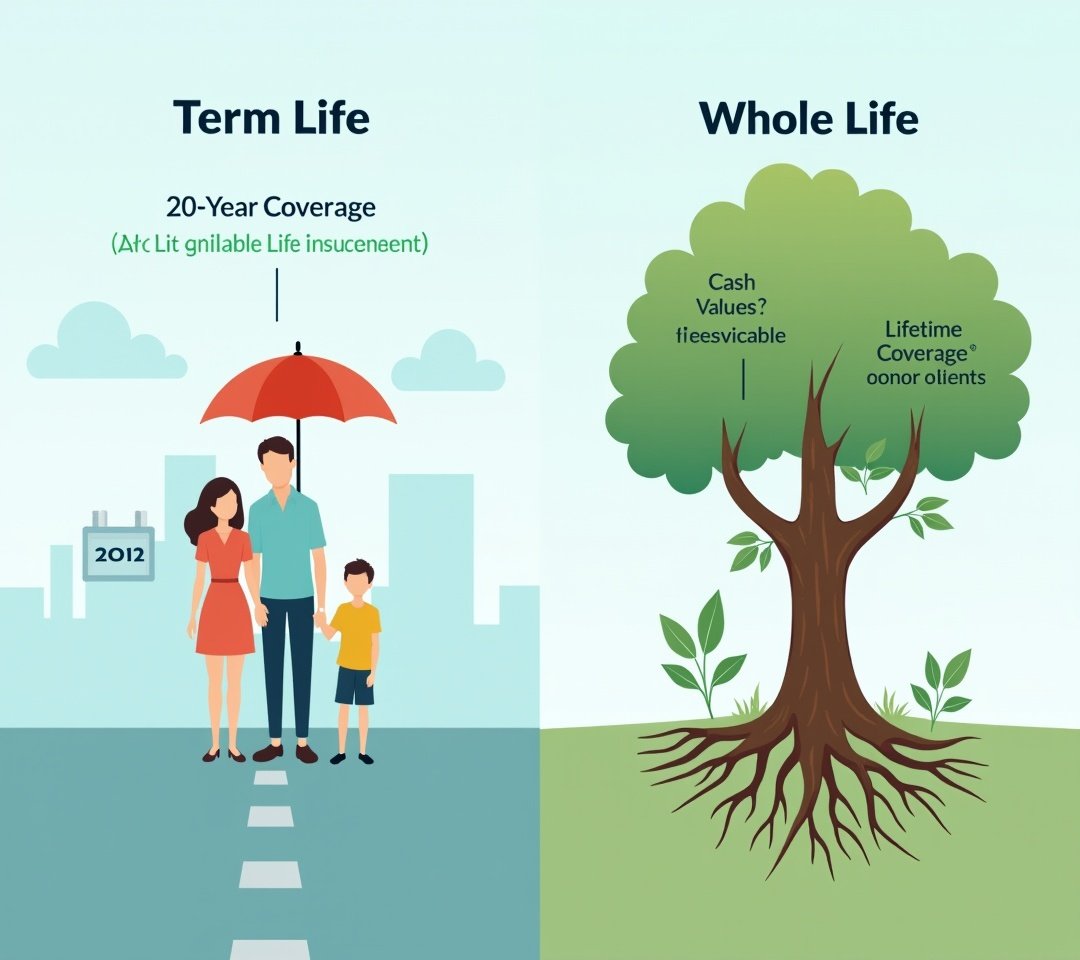

What Even Is Term Life Insurance?

Term life insurance is basically the “rental apartment” of life insurance. You pay premiums for a set period — usually 10, 20, or 30 years — and if you pass away during that term, your beneficiaries get the death benefit. Simple as that.

The beauty of term life is that it’s cheap. Like, shockingly affordable. A healthy 30-year-old can snag a 20-year term policy with a $500,000 death benefit for somewhere around $25-$30 a month, according to Policygenius.

But here’s the catch — once your term expires, you got nothing. No cash value, no payout, nada. It’s pure protection, and honestly, for most young families? That’s exactly what’s needed.

So What’s Whole Life Insurance Then?

Whole life insurance is the “buying a house” equivalent. It covers you for your entire lifetime, and part of your premium goes into a cash value component that grows over time. Sounds amazing on paper, right?

Well, here’s where it gets tricky. Those premiums are significantly higher — sometimes 5 to 15 times more than a comparable term policy. That $280 a month I was paying? A term policy would’ve cost me maybe $35 for the same coverage amount. The cash value growth was also painfully slow in those early years.

Now, I’m not saying whole life is a scam or anything. It has legitimate uses. Wealthy individuals use it for estate planning, and the guaranteed cash value can be a conservative savings vehicle. But for a 28-year-old teacher with student loans? It was overkill.

The Moment I Realized I Picked Wrong

About three years into my whole life policy, my buddy Dave — who’s a financial planner — came over for a barbecue. I casually mentioned my policy and he nearly choked on his burger. He pulled out his phone and showed me what I could’ve been doing instead.

If I had bought term and invested the difference in a low-cost index fund, I would of been way further ahead financially. That’s the classic “buy term and invest the difference” strategy, and for most people in their 20s and 30s, it’s honestly the smarter move. I was so frustrated with myself that night.

When Does Whole Life Actually Make Sense?

Okay, so I don’t want to be completely one-sided here. Whole life insurance has its place, and here are some situations where it genuinely shines:

- You’ve maxed out all other tax-advantaged retirement accounts and want another vehicle for tax-deferred growth

- You have a special needs dependent who will require lifelong financial support

- Estate planning purposes — especially if your estate might be subject to federal estate taxes

- You want a guaranteed death benefit that never expires, no matter what

- Business succession planning or key person insurance needs

If none of those apply to you? Term life is probably your best bet. The National Association of Insurance Commissioners has some great resources for understanding your options too.

Quick Comparison at a Glance

Term life gives you affordable, temporary coverage — perfect for covering a mortgage, raising kids, or replacing income during your working years. Whole life gives you permanent coverage with cash value accumulation, but at a premium price. Most financial advisors will tell you that term is the right choice for roughly 80-90% of families.

What I’d Tell My Younger Self

Look, life insurance decisions are deeply personal. What worked terribly for me might be perfect for your situation, and that’s totally fine. The important thing is that you actually understand what you’re buying before signing anything.

Do your homework, talk to a fee-only financial advisor (not just an insurance agent who earns commission), and think about where you’ll be in 10, 20, 30 years. Your future family will thank you for it. And hey, if you want more straight-talk guides like this one, come hang out with us at Coverage Crafters — we’ve got tons of articles breaking down insurance topics without all the confusing jargon!

Leave a Reply